The following “Chart Elements” are draft definitions of the individual chart segments and principles for use. These definitions will be supplemented by examples and visual illustrations as the project progresses and the new COA is developed.

Last Revised: August 10, 2021 – For updated information related please visit , https://fiscal.gmu.edu/chartofaccounts/

Fund

The Fund is about the Source of Money and associated spending restrictions

- Required = Yes, for all transactions

The Fund segment of the FOAPAL represents the type of money that is being used. Different sources of funding (E&G, Grants and Contracts, Capital Budgets, Restricted Endowments, etc.) have different rules for what can be done with the funds and how they are reported to the state commonwealth and as a part of the Financial Statements. To manage compliance with these rules, different Fund Types are used. Fund Types include, but are not limited to:

- Education and General (E&G)

- Auxiliary Enterprises (AE)

- Externally Sponsored Research Grants & Contracts

- Financial Aid

- Indirect Cost Recovery

- Plant

Within a Fund Type, there can be multiple individual funds for specific purposes. Some funds are general and will be used by a broad range of departments. For instance, the E&G general fund is used by all academic units and most administrative units for their primary operational activities. Other Fund Types are subdivided with a hierarchy to categorize numerous project-specific unique fund codes. New funds will be established when the funding must be reported on separately and balances must be tracked without regard to the university’s fiscal year. For example, Grants and Contracts, and Capital Projects require reporting on each separate source of funds, and therefore each grant or project will have its own fund number.

As a general rule, any funding source that needs to be tracked across multiple fiscal years should be a separate Fund. Banner’s functionality maintains separate fund balances (meaning the remaining balance from actual inflows and outflows carries forward from one fiscal year to the next) by Fund, but not by Organization. A common example would be grants/contracts where the lifecycle of the grant often does not align with the university’s fiscal year.

Fund Segment Hierarchy Principles

UPDATED, August 6, 2021

To maintain consistency across the University for standardized and consolidated reporting/analysis, best practices suggest that each level of the hierarchy for the Chart of Accounts should represent “like” items.

- Fund Type Level 1:

- This follows industry standards for financial management, dividing funds into Unrestricted, Restricted, Loan, Plant, etc.

- Fund Type Level 2:

- This level contains more Mason-specific fund groupings, such as Education and General, Indirect Cost Recovery, Carryforward. This is the level at which rules can be applied regarding the fund type, such as whether the funds carry over year to year, default override rules, and whether sufficient funds will be checked.

- Level 3:

- This is the first level of the predecessor values in Banner. This level breaks down the Mason specific groupings in Fund Type Level 2 into groups for reporting purposes. For example, Carryforward breaks into Pool, Startup, Self-Supporting, etc.

- Level 4: University-Wide Funds

- Some funds will continue to be University-wide funds (E&G, Student Loans). These funds are allocated to the University as a whole, and will remain in a single fund. They may be budgeted across multiple organizations, but they act as a whole unit for purposes of reporting to the state or other entities. These funds will remain at L4. Another term for this group is “Organization-driven” funds – the Org is the primary driver of the FOAPAL defaults for these funds and many Orgs will associated with a single Fund.

- Other funds will continue to the Level 6 – for these L6 Funds, L4 would be another level of grouping, for example, in Grants, it breaks the Federal and Non Federal into specific sponsors.

- Level 5: Department Funds

- Some funds will be Department-level funds. Examples include unit specific Auxiliary Enterprise funds, such as fund balances for Housing, Dining, and the Child Development Center. These funds will also be “Organization-driven” funds, where the Org is the primary driver of the FOAPAL string with the Fund value defaulted in based on the Org. Many orgs may be associated with a single Fund.

- For funds that continue to Level 6, Level 5 is another level of grouping, for example, Specific Sponsors are broken into Grants versus Contracts at this level. For some funds, L4 and L5 may be redundant.

- Level 6:

- This is the level at which transactions will be recorded for the specific funds. This level contains individual Grants and Contracts agreements, Pool funds, Internal research, Seed funding, Startups, etc. They generally either carry over year to year, or have inception-to-date reporting. They carry their own rules, purposes, and responsible individual (Principal Investigator, Faculty member). These could be called “fund-driven” – the Fund in these cases are the primary driver of FOAPAL with the Org value defaulted based on the Fund. Each of these funds will generally only be associated with a single Org.

Organization

The Organization (Org) is the “Who” – Who is responsible for the financial activity

- Required = Yes, for Revenue and Expense transactions, otherwise optional

The Organization (“Org”) segment of the FOAPAL should reflect the financial organizational structure of the University and align with the operational academic structure. This means that organizational units or departments should be represented by a unique Org number and that the hierarchy for how Orgs are grouped for reporting should reflect the reporting structure of the institution (e.g., Departments roll up to a College/Division, which in turn roll up to the Provost/SVP, etc.). See separate principles related to hierarchy levels and definitions (to be developed). Transactions are recorded at a lower level in the hierarchy (L6 level), within the department or program responsible for managing to their approved budget.

An Organization may be funded by multiple sources (identified by different Funds) and be associated with multiple Programs, Activities, and Locations. The Organization can be used in reporting to display the financial status of the entire department, including all types of financial activity that the department is responsible for (E&G, Grants, Start-Ups, Indirects, etc.)

Organizations should be established for cost centers that have:

- Budgets

- Financial transactions (salaries/purchasing)

- A single individual responsible for the financial health and decision-making of the organization (even if there is a higher-level approver) – this person will be named as the Financial Manager for the organization in the system

- A tie to an administrative division or academic department or program that can be identified in the University hierarchy.

Organizations should NOT be established for:

- Reporting purposes alone

- Activities (example: tracking one type of business of the university, like “Department Research” or “Fall Festival”)

Organization Segment Hierarchy Principles

UPDATED, August 6, 2021

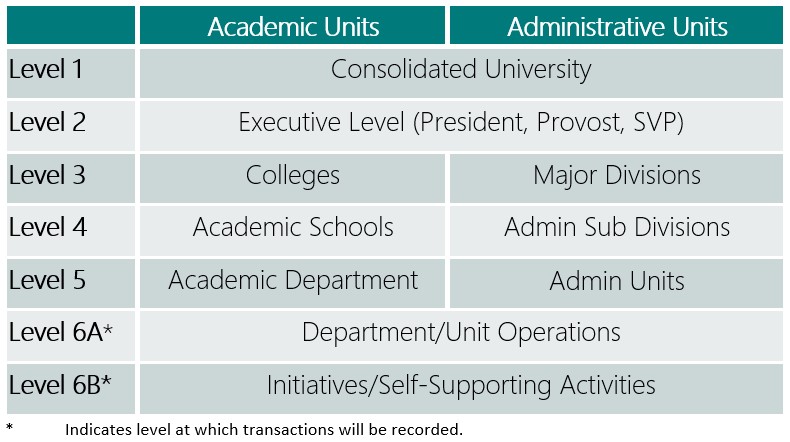

To maintain consistency across the University for standardized and consolidated reporting/analysis, best practices suggest that each level of the hierarchy for the Chart of Accounts should represent “like” items. For the Organization segment, which is intended to represent the organizational operating structure of the University, the proposed organizational unit represented by each level is listed in the table below:

Note that while there are structural differences between the Academic and Administrative sides of the structure, comparability is maintained — particularly at the highest and lowest levels of the hierarchy. Some branches of the hierarchy with less organizational complexity will see redundancy between the levels as described below. The value in placing “like items” consistently at the same level is supporting meaningful reporting with capability to drill down into more granularity when appropriate. We can also use a specified level for consistent internal control points with across the institution.

- Level 1:

- This will always represent the consolidated institution and is used for reporting in the Financial Statements, to the BOV, and others on Mason’s complete financial operations.

- Level 2:

- The University is led by an Executive team – several functions report directly to the President, while the Provost and the Senior Vice President for Finance and Administration each lead the Academic and Administrative operations, respectively, of the institution. These three areas of executive responsibility are reflected at Level 2.

- Level 3:

- Within each of the three executive “verticals”, there are major subdivisions – either individual Colleges on the Academic side (e.g., CHSS, COS), or major operational units on the Administrative side (e.g., Facilities, ITS).

- Level 4:

- Academic: Each College will have a Level 4 (L4) unit to represent the roll-up for College Administration and Student Services (e.g., Dean’s Office, Student Advising, etc.) and an L4 for College-level Centers and Institutes, if applicable.

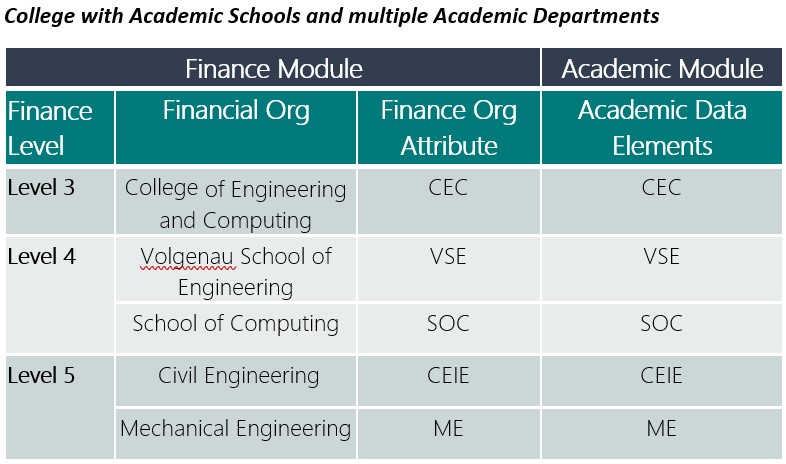

- Some Colleges have Academic Schools within the College (e.g., College of Engineering and Computing (L3) has the Volgenau School of Engineering and the School of Computing) which will be represented at L4 of the hierarchy.

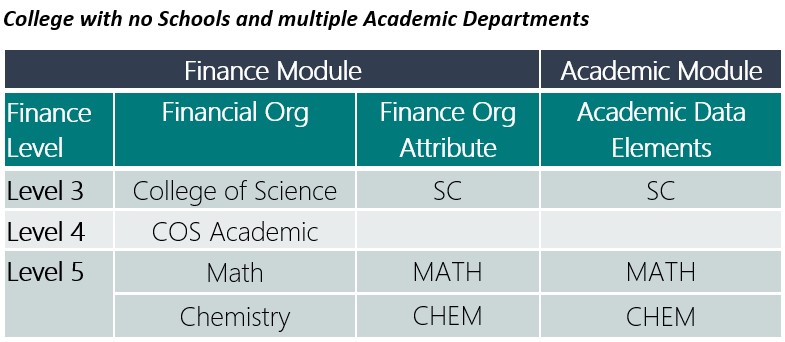

- Colleges that do not have separate Schools within the College (College of Science L3) will have an L4 roll-up for all academic activities. (COS Academic Activities L4).

- Administrative: Within the Administrative side of the organization, some Major Divisions have distinct operational Sub-Divisions (e.g., Business Services and Operations includes Business Services, Mason Police, etc.). These sub-divisions will be represented at Level 4 of the hierarchy. Divisions that do not have the same level of complexity will see redundancy between Level 3 and Level 4 groupings.

- Academic: Each College will have a Level 4 (L4) unit to represent the roll-up for College Administration and Student Services (e.g., Dean’s Office, Student Advising, etc.) and an L4 for College-level Centers and Institutes, if applicable.

- Level 5:

- The organization structure of both Academic and Administrative Divisions contain multiple operating units or Departments. These operating units may have one or more operational sub-units within.

- For those with multiple units, Level 5 will serve as a roll-up of those units (which will be Level 6A).

- For those with only one unit, there will be redundancy between Level 5 and Level 6.

- The organization structure of both Academic and Administrative Divisions contain multiple operating units or Departments. These operating units may have one or more operational sub-units within.

- Level 6A:

- This is the level at which most transactions are recorded for both Academic and Administrative units. As noted above, Departments that have multiple operational units (e.g., Fiscal Services L5) may have multiple L6A Orgs (Accounts Payable, Student Accounts, General Accounting, etc.). Other Departments may have only one transaction L6A Org value. For Academic Departments, generally there will be one 6A Org, but additional 6A orgs may exist for departmental research centers or major facilities that have their own operating structure.

- Level 6B:

- Some units may have a need for even more granular tracking. For example, Global Education Office runs programs for study abroad. The individuals responsible for those programs manage the funds associated with them. We envision these individual programs existing at Level 6B in the hierarchy and rolling-up to a Level 6A “predecessor” or ‘parent’ org. (Note: The level retains “6B” rather than “7” to indicate that it is a 6-character value.)

Alignment of the Financial Hierarchy for Academic units to the Academic Data Elements in Banner:

The Academic data tables in Banner (i.e., those for recording course, registration, student, etc.) do not interact directly with the financial chart of accounts and related hierarchies. However, there is value in aligning the Academic operational data structure with the financial data structure to enable reporting and analytics that combine information from both sources for more meaningful information.

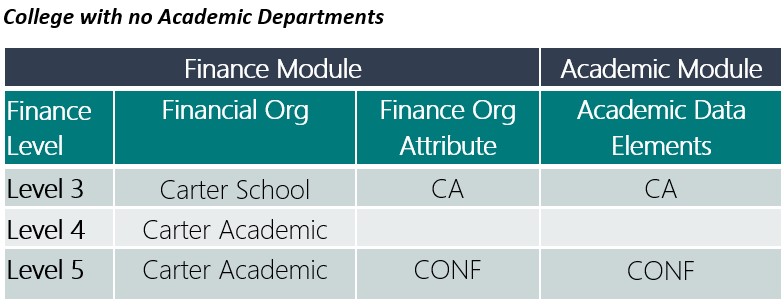

The Academic data structure includes tables that define Colleges, Divisions, and Departments. We propose aligning these three data components with Levels 3-5 of the Organization segment of the financial COA hierarchy:

Although we sometimes refer to these data elements as the “Academic Hierarchy”, the data tables where these are defined in Banner are independent and do not enforce a strict hierarchy in the same way that the financial chart does. The Department values are not assigned to a single predecessor Division, which in turn are not assigned to a predecessor College. Despite this lack of enforced hierarchy, we can establish expectations and rules for the assignment of Departments to Divisions, and Divisions to Colleges which can be monitored for consistency via standard reporting tools.

The usage of College, Division, and Department values appears throughout Banner. College and Department fields are used in multiple places in Banner tables, including Courses, Student Enrollment, Academic Program Major, and Faculty Load. Division is not widely used – it primarily appears only on Course records.

To embed the alignment between Academic and Financial hierarchies within Banner, we are exploring adding an attribute to support automated reporting.

Recording this relationship within Banner will require communication between offices with responsibility for maintaining the respective data elements in Banner, which will also help us to maintain consistency of the interrelationships over time. Storing the information within Banner and incorporating it into the datamart load will allow us to leverage the information for consistent reporting without maintaining custom tables outside of the ERP. The combined data elements will enable multiple reporting/analytics such as cost/revenue by credit hours, average revenue/cost per student, and ratio comparisons across programs.

Account

On operating reports of revenues and expenses, the Account segment of the FOAPAL represents what the money originated as (e.g., tuition, appropriation, fees) or what the money is being spent on (salaries, supplies, travel). On the balance sheet, the Account segment identifies what the asset is made up of (e.g., cash, equipment, land) or what the obligation is for (e.g., trade accounts payable, accrued interest, debt). Accounts are organized into the following Account Types:

- Assets

- Liabilities

- Control

- Net Assets

- Revenue

- Expense

- Transfers

Accounts also have a hierarchy to facilitate grouping like accounts into summarized information for reporting (e.g., salaries, fringe, contract services, travel).

An Account can be established when there is a University-wide need to track or establish rules for a particular type of transaction that cannot be identified by other attributes of the transaction. For example, if there is a reporting requirement to track foreign travel separate from domestic travel, this would necessitate a separate Account being created. Similar requirements exist for grant expenses that have indirect costs applied versus those that do not. However, tracking Central Office Supplies versus Academic Supplies would not require separate accounts, as that information could be determined by other segments of the chart.

Program

The Program segment of the FOAPAL represents the function of the University that the transaction supports. Why expenses are incurred relates direction to the mission of the university and programs are used for Financial Reporting. “Programs” in the context of the COA are not equivalent to “academic programs” such as degree programs or specific academic disciplines. These are also referred to “functional” expense categories for financial reporting. Programs include:

- Instruction

- Academic Support

- Institutional Support

- Net Assets

- Various types of Research

Program codes directly support financial reporting requirements and therefore programs will not be created unless there is a regulatory need. Where possible, default Program codes will be assigned to Fund or Organization values to support consistent and meaningful reporting.

Activity

The Activity segment (the second A) in FOAPAL is an optional segment that can be used fairly flexibly to track work within or across the organization(s). In our earlier example of what would not require an organization, our “Fall Festival” would be a good example of an activity. If multiple organizations participate in the Fall Festival, they could use an Activity code to track all activity related to the Fall Festival to understand all the costs associated with it across the university. Individual departments may also establish activity codes for groups of expenses unique to their operation which they cannot track in other ways.

When a new Activity code is requested, Fiscal Services will determine if the expenses could be grouped using any other attributes available in the system. If the grouping is truly unique, the request will be approved.

Note that the use of an Activity code requires all responsible departments to remember to use the Activity code on all appropriate transactions, so it should be well-communicated and there should be a shared understanding of when to use it. Usage of Activity codes are the responsibility of the department or group requesting the code, and will not be administered by Fiscal Services.

Location

The Location segment of the FOAPAL represents the place the transactions are happening. This is also an optional segment, meaning that the system will not require it to be populated on transactions. In some circumstances, it may be helpful to know which campus or off-campus facility is related to the transaction. This can enable reporting of the expenses related to a specific campus or building and can also help understand the growth of different areas of the University..